The shift from traditional group plans to the Individual Coverage HRA (ICHRA) is no longer a "future" trend. As of 2026, about half of all brokers are currently selling ICHRA. And of those selling ICHRA, nearly a quarter have scaled to 11+ clients on ICHRA.

Still, that leaves many brokers asking the question: "How do I sell ICHRA to my employer clients?"

Knowing what an ICHRA is and knowing how to sell ICHRA at scale are two different things. If you want to move from a single sale to a scalable practice, here is your guide to selling ICHRA.

Want the exact scripts and checklists featured in this guide? Download the Zorro Broker Sales Playbook and start scaling your ICHRA practice today.

But first, the basics: What is ICHRA?

Before you can start selling effectively, you need to perfect your pitch — and that starts with understanding ICHRA inside and out.

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is a flexible health benefit that allows employers of all sizes to provide tax-advantaged reimbursements for individual health insurance premiums and qualified medical expenses. Instead of offering traditional group health coverage, employers set a defined contribution amount, and employees choose the individual health plan that works best for them and their families.

Key benefits of ICHRA for employers

When selling ICHRA to employer clients, focus on these compelling advantages:

→ Cost control and predictability: Employers escape the cycle of unpredictable double-digit renewals. With ICHRA, they set their contribution amount and know exactly what their benefits budget will be year over year.

→ Flexibility: ICHRA allows employers to create different contribution levels for up to 11 employee classes — by geography, full-time vs. part-time status, salaried vs. hourly workers, and more.

→ Risk elimination: For employers tired of being in the "risk business," ICHRA provides a clean exit strategy.

→ Competitive talent advantage: Employees can select plans that include their preferred doctors and medications, and if they change jobs, they can continue the same coverage.

→ Tax advantages: ICHRA reimbursements are tax-free for employees and tax-deductible for employers.

Who is a good fit for ICHRA?

Scaling starts with knowing where ICHRA makes the most sense. You aren’t looking for every group; you’re looking for the Ideal Customer Profile (ICP) where the math and the culture align.

The best candidates for ICHRA in 2026 are employers with one or more of these traits:

- High renewals: Groups seeing consistent double-digit increases

- Geographic complexity: Workers spread across multiple states or regions

- Risk fatigue: Leadership tired of claims-based pricing volatility

- Workforce mix: A blend of salaried and hourly workers

- High turnover: Industries where portability is a competitive advantage

- First-time benefit offerers: Companies that recently became ALEs under the ACA

- Cost-sensitive organizations: Nonprofits, franchises, and businesses on tight margins

- Seasonal or variable workforces: Hospitality, retail, contact centers

- Remote-first companies: Distributed teams across multiple states

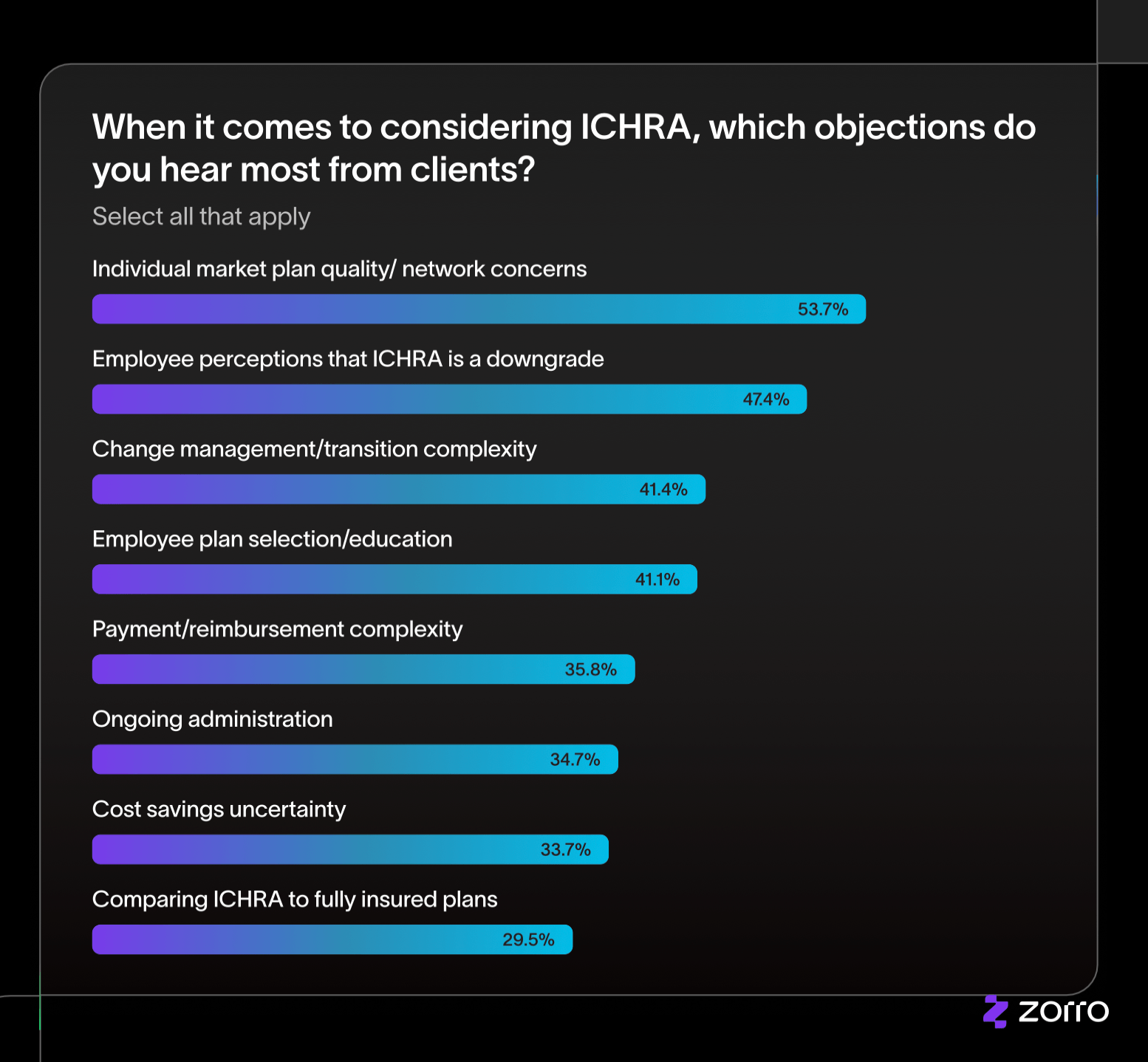

What are the most common objections to ICHRA?

Brokers selling ICHRA often come up against objections from employers. After all, ICHRA is still relatively new — and new health insurance strategies can come with uncertainty.

According to our 2026 Broker ICHRA Survey Report, the most common objections to ICHRA are rooted in concerns around individual market plan quality, employee satisfaction, and change management.

If you take a closer look at these objections, you might notice a pattern: almost none of them are about the ICHRA model itself, but rather about implementing and managing ICHRA. In other words, it’s not about the what but the how. Understanding this nuance makes it much easier to overcome objections.

How to address and overcome any ICHRA objection in four steps

In our recent webinar on Selling ICHRA in 2026, our VP of Sales, Jeff Kirchick, broke down his tried-and-true process for addressing and overcoming ICHRA objections. Use these ICHRA sales tactics to move prospects from hesitation to action.

According to Jeff, when it comes to ICHRA, "the sale starts at NO". By that, we mean that objections can reveal more about their fears and priorities — which opens the door to more targeted selling techniques.

Jeff teaches a four-step framework for handling objections systematically. Let's walk through how to apply each step when selling ICHRA.

Step 1: Isolate the concern

Before you can address an objection, you need to know if it's the only thing standing in the way. The question to ask is: "Is that your only concern?"

As Jeff puts it: "It's okay if it's a long list. I'd rather know that there's 10 things than think that there's one and spend a big chunk of time helping someone feel better about that one thing, only to find out that there were nine other things."

Step 2: Test the concern

Once you've isolated the concerns, test whether they're real deal-breakers or just surface-level hesitations.

How to test: Remove the objection hypothetically and see if they'd move forward.

For example, if someone says "ICHRA is too expensive," you'd say: "Okay, hypothetically, if it was free, would you move forward right now?" If they say, "Well, no... I'm also worried about the change management," then you've learned that pricing was not their only concern. By getting a more holistic understanding of their concerns, you’ll be in a better position to address them effectively.

Step 3: Narrow the concern using labeling, mislabeling, and mirroring

Broad concerns like "change management" or “servicing” are nearly impossible to overcome because they're too vague. Your goal is to peel back the layers until you reach the specific, narrow fear underneath, using these three techniques:

1. Labeling – Reflect their emotion back to encourage them to elaborate

- Employer: "I'm worried about servicing."

- You: "It sounds like you're worried your employees might not get the help they need if something goes wrong during enrollment."

- Employer: "Yeah — we've had bad experiences in the past where our team had to step in because the vendor didn't follow through."

Now you know this is about trust after poor experiences with past vendors — not servicing in general.

2. Mislabeling: Slightly exaggerate to force them to narrow their stance

- Employer: "I'm worried about change management."

- You: "It seems like you're not confident your team can handle any change at all."

- Employer: "Well, no — that's not it. It's just that we've already got a lot on our plate, and switching benefits feels like it could overwhelm HR."

Now you've uncovered the real objection: bandwidth and employee confusion.

3. Mirroring: Repeat their exact words back as a question

- Employer: "Aetna is leaving the individual market."

- You: "Leaving the individual market?" (pause)

- Employer: "Yeah — if Aetna won't stay in it, I'm worried employees won't have good options."

- You: "Good options?" (pause)

- Employer: "Exactly. We can't risk disruption mid-year or have people forced to switch networks."

Step 4: Get them to say "yes" to the outcome (before they say "yes" to ICHRA)

Once you've narrowed the concern (Step 3), try to paint a hypothetical picture where that concern doesn't exist and ask if they'd move forward:

- Employer: "I'm really just worried that the employees won't know how to select a plan."

- You: "Hypothetically, if we could show you that your employees will be able to select a plan, and that whatever frustration there is will be minimal and short term — would you otherwise be excited about all the benefits you'd be getting in return?"

If they say yes, you've shifted the burden from "convince me to do ICHRA" to "show me you can handle this one specific thing."

Asking "And Then?" to defeat the "Scary Monster"

Many buyers freeze because they imagine a catastrophic outcome — we call that the “Scary Monster.” But when you ask them to walk through what would actually happen step by step, they often realize the risk is manageable.

For this, Jeff recommends another powerful tactic: asking "And Then?" repeatedly to help employers follow their fears to their logical conclusion.

- Employer: "The employees might get confused." And then?

- You: "Are they more confused than when you switched HRIS systems? Did everyone quit, or did they figure it out in a few days?"

- Employer: "I'm worried employees will have to deal directly with the carrier." And then?

- You: "Will the carriers not answer the phone? Will everyone have low morale? Or is this just going to result in employees having to spend some of their time on something?"

“Sometimes the scary monster is real,” Jeff explains. “But you don't know until you ask this question whether it's real or whether it's somewhat maybe in their mind that they need to think it through."

Combat indecision using the JOLT effect

Most lost ICHRA sales are not lost to competitors, but to indecision. To HR decision-makers and CFOs, transitioning to ICHRA can feel like a big leap from traditional group plans. After all, the status quo may be more comfortable, even if it's not what's best for their budget or employees.

The JOLT framework complements the four-step objection handling process by specifically addressing indecision:

→ J - Judge the indecision: Determine if the client has a "pain" problem (cost) or a "confidence" problem regarding compliance or employee choice. Is the CFO risk-averse? Is HR overwhelmed?

→ O - Offer a recommendation: Don't ask what they want to do; tell them what they should do. "Based on what you've told me — renewal volatility, multi-state expansion, and HR admin overload — I recommend moving to an ICHRA structure with X class strategy and Y contribution modeling."

→ L - Limit the exploration: Too many options cause paralysis. Jeff warns: "The problem is that it actually creates a second inflection point where the client or the employer feels like they can mess up." Don't show 30 scenarios. Narrow it down to the two best options based on their goals.

→ T - Take risk off the table: Show census validation processes, compliance safeguards, AI plan decision support, implementation checklists, and case studies. "Here's what typically goes wrong in ICHRA transitions — and here's how we prevent each one."

Selling ICHRA in 2026 is about becoming a "decision simplifier"

By focusing on the right ICP and using advanced objection-handling tactics, brokers can move away from reactive renewals and toward a proactive, scalable business model.

The brokers who will win in the ICHRA space aren't those who simply know what ICHRA is or how it works mechanically. They're the ones who have mastered the art of guiding employers through fear and indecision toward confident action.

With the right approach, ICHRA can transform from a hard sell into a natural solution for employers facing the challenges of 2026's benefits landscape.

Missed Jeff’s ICHRA Sales Masterclass in action? Watch the webinar on-demand here.

Looking for more tactical guidance on ICHRA sales? Download our official Zorro Broker Sales Playbook!

Q&A

Question: What is ICHRA and why is it gaining traction in 2026?

Short answer: An Individual Coverage HRA (ICHRA) lets employers of any size reimburse employees tax-free for individual health insurance and qualified medical expenses instead of offering a traditional group plan. Employers move from a defined benefit to a defined contribution model — setting predictable budgets — while employees choose plans that fit their needs.

Adoption is accelerating because the individual market has matured: ACA marketplace enrollment grew 113% from 2020–2025, cost trends in the individual market were 26% lower than employer-sponsored coverage (2018–2024), more carriers are competing, and ICHRA offers geographic flexibility for multi-state workforces.

Question: Which employers are the best fit for ICHRA?

Short answer: Target groups where the math and culture align. Ideal profiles include employers with: high or volatile renewals; multi-state or geographically dispersed teams; leadership tired of claims-driven risk; mixed workforces (hourly/salaried, part-time/full-time); high turnover where portability helps; first-time benefit sponsors (e.g., new ALEs); tight budgets (nonprofits, franchises); seasonal/variable staffing (hospitality, retail, contact centers); and remote-first companies spread across states.

Question: What benefits should I emphasize when pitching ICHRA to employers?

Short answer: Focus on outcomes that matter to executives and HR:

- Cost control and predictability: set contributions and avoid double-digit renewal surprises.

- Flexibility: tailor contributions across up to 11 employee classes (e.g., geography, status, pay type).

- Risk elimination: exit claims volatility and stop “being in the risk business.”

- Talent advantage: employees pick plans that fit their doctors/meds and can keep coverage when changing jobs.

- Tax advantages: reimbursements are tax-free for employees and tax-deductible for employers.

Question: How do I handle common employer objections about ICHRA?

Short answer: Use the four-step framework:

- Isolate: ask, “Is that your only concern?” to surface the full list.

- Test: remove a concern hypothetically (“If cost weren’t an issue, would you proceed?”) to reveal the real blocker.

- Narrow: turn broad fears into specific, solvable ones using labeling (reflect emotions), mislabeling (slight exaggeration to refine), and mirroring (repeat key words as a question).

- Secure outcome agreement: get a “yes” to the desired outcome before a “yes” to ICHRA (“If we can ensure simple plan selection with minimal disruption, would you move forward?”). This shifts the ask from “buy ICHRA” to “solve this one defined risk.”